Research & Publications / Decoding Energy News

DEN 8 | The Oil & Gas Industry's Pivot to a Sustainable Future

The Oil & Gas Industry's Pivot to a Sustainable Future

The oil and gas industry is undergoing a fundamental transformation as it shifts from conventional fossil fuels to a more sustainable energy mix, driven by EU directives. The transport sector is a significant contributor to EU Greenhouse Gas (GHG) emissions, accounting for 30.9% [Greenhouse gas emissions by country and sector, European Parliament] of the total. Specifically, domestic transport, international aviation, and international shipping are responsible for 23.8%, 3.2%, and 3.9% of these emissions, respectively. This transition is no longer a matter of "if" but "how fast," driven by environmental obligations, technological advancements, and a growing consensus on the need to mitigate climate change.

While hydrocarbons remain the backbone of the global energy system, a new generation of greener alternatives—such as Sustainable Aviation Fuels (SAF), biofuels, synthetic fuels, and Recycled Carbon Fuels (RCFs)—is emerging as a key player in the decarbonization effort. Regulatory frameworks, such as the EU Emissions Trading System (ETS II), are also reshaping the cost and competitiveness of fuels, creating new challenges and opportunities for refineries and end-users alike.

The Rise of Greener Fuels

Biofuels, derived from biomass and biogases from organic matter like plants, algae, and waste, are at the forefront of this transition. Unlike hydrocarbons, they are part of a "closed loop" carbon cycle, which significantly reduces net lifecycle GHG emissions.

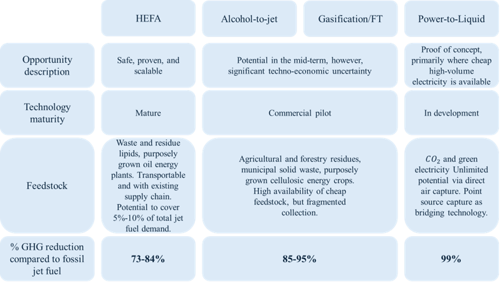

With the ReFuelEU Aviation directive (established in July 2021), the share of fuels from SAF in EU airports is set to grow from 2% in 2025 to 70% by 2050. Designed to replace conventional jet fuel, SAF can reduce carbon emissions by up to 80% [International Air Transport Association (IATA)] on a lifecycle basis and can be used in existing aircraft and airport infrastructure without modifications. SAF is made from sources such as used cooking oil, animal fats, municipal solid waste, and agricultural residues, making it a powerful tool for decarbonizing a sector that's difficult to electrify.

In road transport, Bioethanol (made from crops rich in sugars and starches) and biodiesel (produced from vegetable oils) help lower emissions from cars and trucks. Advanced processing can even convert these fuels into SAF, expanding their strategic importance.

Marine Fuels and the Low-Sulphur Challenge

The shipping sector is also undergoing a profound transformation following the IMO 2020 regulation, which capped the sulfur content in marine fuels at 0.5% [International Maritime Organization (IMO)] (outside Emission Control Areas). This regulation has forced a global shift toward very low sulfur fuel oil (VLSFO) and marine gasoil (MGO). High sulfur fuel oil (HSFO) is now mainly used in vessels equipped with scrubbers.

For countries with significant maritime activity, such as Greece, this shift has created new challenges for refineries. They must adapt their product slates and invest in more complex refining processes to stay competitive in the international bunker market, as demand for low-sulfur alternatives has replaced the historical demand for high-sulfur fuel oil.

The Role of ETS II in Fuel Economics

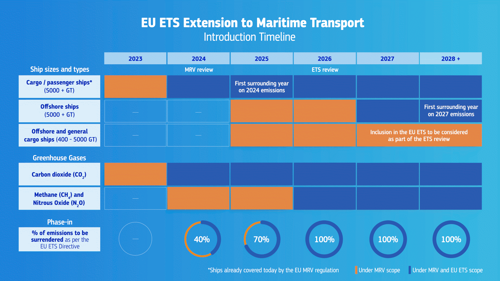

The EU ETS II, which will cover the transport and building sectors starting in 2027, represents a paradigm shift in carbon pricing. It will directly affect road, marine, and heating fuels, creating carbon cost pass-throughs that will significantly reshape end-user prices.

For aviation, costs are already tangible, as intra-EU flights are covered by the original ETS and will increasingly rely on SAF blending mandates. For shipping, ETS II introduces a cost on marine fuels supplied in the EU, phased in between 2024 and 2027. This will drive demand for low-emission alternatives while penalizing conventional marine fuels, accelerating the transition but also intensifying cost pressures for refiners and consumers.

A Greek Perspective: Tourism, Shipping, and Refining Challenges

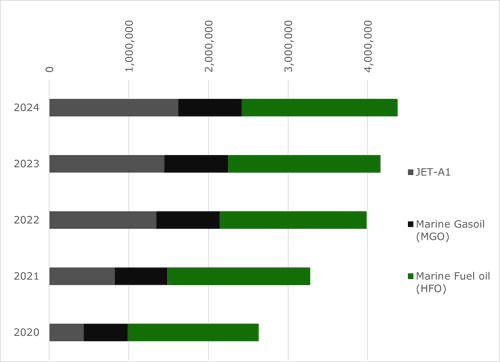

Greece stands out as a unique case in Europe’s fuel transition. Its energy profile is characterized by a very high demand for marine fuels, due to its global shipping dominance, and aviation fuels, linked to its booming tourism sector. During peak summer months, jet fuel demand surges, while year-round, Greece remains a top bunkering hub in the Mediterranean.

This dual demand for bunker and jet fuel presents both an opportunity and a challenge for Greek refineries. They must secure competitive access to SAF and low-sulfur marine fuels to serve their markets and align with EU climate legislation. This is challenged by the need to shift away from high-sulfur fuel oil production, which historically represented a large share of their output.

As the combined pressures of IMO regulations, SAF mandates, and ETS II compliance intensify, Greek refiners are forced to rethink their long-term strategies, balancing traditional hydrocarbon exports with investments in bio-refineries, feedstock diversification, and advanced conversion units.

A Stark Cost Comparison: The Price of Green

While the environmental benefits are clear, the economics of this transition present a significant challenge. Currently, greener fuels are substantially more expensive than their conventional counterparts.

The price of conventional fuels is driven by volatile global crude oil markets, refining costs, seasonality, and geopolitical factors. Despite price volatility and rising costs for consumers due to new EU directives and ETS prices, they benefit from a century of massive investment in infrastructure and production, which keeps their costs relatively low.

The cost of sustainable fuels is heavily influenced by the price and availability of their feedstocks, as well as the high capital costs of production facilities, making them significantly more expensive than hydrocarbons.

SAF is a prime example, often priced at 2-5 times the cost of conventional jet fuel [IATA], currently averaging 4.2 times more. These costs are closely related to limited production scale, high feedstock expenses, and regulatory compliance fees. While government incentives and subsidies are helping to close this gap, the price premium remains a major barrier to widespread adoption. Similarly, biodiesel can be 0.7-1.3 times more expensive than conventional diesel [Energy Policy, Importance of biodiesel as transportation fuel]. Bioethanol, while not considerably more expensive than gasoline, requires 1.5 times more fuel to achieve the same efficiency [U.S. Department of ENERGY, Ethanol Fuel Basics]. These higher costs are often passed on to consumers or subsidized by governments to meet renewable energy targets.

Recently, the EU announced a new €2 billion funding scheme for sustainable fuels under the EU ETS. This package could underwrite 216 million liters of SAF, offering up to €6/liter for e-fuels and €0.5/liter for biofuels to airline companies [IATA]. The price disparity is a key reason why SAF and other biofuels currently make up a minuscule fraction of total fuel consumption in their respective sectors.

The Path Forward

The transition from conventional to greener fuels is a long-distance marathon. While the initial costs of biofuels, SAF, and RCFs are high, economies of scale and technological maturity are expected to drive prices down over time. Meanwhile, EU funding, such as the recent €2 billion package, provides a critical push for scaling up production.

For Greece, the challenge is particularly acute, as its simultaneous reliance on aviation and marine fuels makes the country a test case for how refineries in Europe must adapt to a future where carbon costs, low-sulfur requirements, and renewable fuel quotas converge.

Ultimately, the race to a net-zero future is not about abandoning the past but about reinventing the future of refining and fuels. Greece, with its strong refining capacity and strategic location, has the potential to become a regional leader in sustainable fuels, provided it can seize the momentum of regulatory change and turn it into industrial opportunity.