Newsroom / Center News

The Paradox of the Greek Electricity Market

The Market Landscape

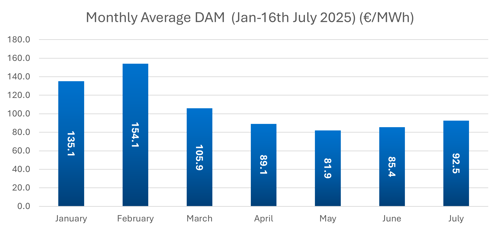

Greece’s electricity market in 2025 exhibits a paradox: while wholesale prices have improved due to increased renewable energy penetration and relatively stable natural gas costs, end-users—both industrial and residential—continue to pay among the highest final prices in Europe. During the first 7 months of 2025, spot prices on the Hellenic Energy Exchange averaged around 106.8 €/MWh, a significant decline from mid-2024 levels when peak-day prices frequently approached €200/MWh. More specifically, the spot market prices averaged 135.1 in January and decreased to 92.5 in July.

Even under elevated cooling demand during heatwave conditions, prices remained below €140/MWh, a performance largely driven by the merit-order effect of expanded solar photovoltaic generation during midday and the stabilizing influence of gas price dynamics. The increased real-time share of zero-marginal-cost RES output suppresses marginal clearing prices in those intervals, yet these wholesale gains are not proportionally reflected at the consumer level.

The divergence arises from systemic frictions, particularly within balancing and settlement mechanisms, as well as from temporal mismatches between generation and demand. Balancing costs—incurred to resolve real-time deviations and maintain frequency and adequacy—have escalated sharply, projected to exceed €1 billion in 2025. Available evidence suggests this escalation cannot be fully attributed to technical necessities like variability or inertia loss; rather, it points to structural distortions, opaque procurement and allocation practices, and misaligned incentives in how imbalances are priced and settled.

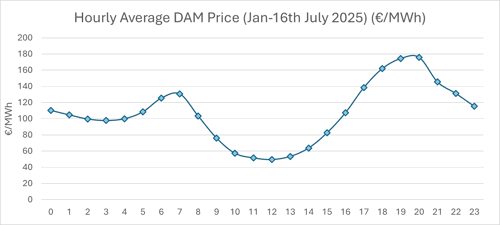

Simultaneously, intra-day price volatility exacerbates inefficiency: abundant low-cost solar generation during midday suppresses prices temporarily, but as insolation wanes in late afternoon and early evening while demand stays high, the system reverts to higher-marginal-cost thermal resources. Spot prices during those evening hours spike even absent extraordinary events, and because retail billing aggregates or averages across these intervals, the value of cheap green energy is diluted. To illustrate this point, on average for the time period in discussion, the lowest price occurred around 12 noon reaching 49.5 €/MWh, while the highest was recorded at 8 p.m. reaching 175.9 €/MWh.

Mitigating the Risks

A technically sound mitigation pathway exists in the form of energy storage and broader flexibility integration. Utility-scale battery systems, notably lithium-ion deployments with rapid charge/discharge response, can time-shift surplus midday renewable output to peak evening demand, reducing reliance on expensive gas-fired peaking capacity and dampening price spikes. Storage performs arbitrage that smooths the supply-demand curve, firming the contribution of variable RES and alleviating the “evening bill” distortion.

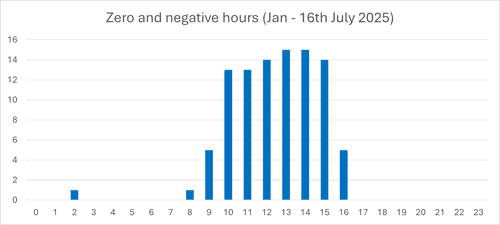

This would also mitigate the phenomenon of the “duck curve”, that also leads to zero, or even negative, spot prices. To put things into perspective regarding this effect, for the period of January to July, the DAM prices fell to, and even below, zero for a total of 96 hours, with most of these hours taking place during midday, when the PV generation is at its peak. This translates to a percentage of 2% of the total hours in the same time period.

However, the actual system impact of emerging storage capacity in 2025 depends critically on the clarity and design of regulatory and market participation frameworks: uncertain compensation structures, ambiguous rules for bidding into energy, balancing, or capacity markets, and poorly defined revenue streams for provision of firmness and ancillary services risk underutilization of these assets despite their theoretical value.

In any case, the conclusion is the same. Without structural reform, specifically, a transparent and efficient redesign of balancing settlement, the creation of predictable and accessible value streams for storage and flexibility, and incentive alignment across wholesale, retail, and system-security layers, Greece risks entrenching high consumer costs and eroding industrial competitiveness even as wholesale fundamentals improve. The current market architecture externalizes transition costs to end-users, fails to fully redeem the value of renewable injection, and permits temporal price mismatches to persist unmitigated.